Beneath the Bubble, the Void

There's a growing tension in the financial plumbing of the United States — subtle but significant. While equity indices remain near all-time highs, valuations are stretched, and credit spreads stay tight, the short-term funding system is quietly flashing amber.

The U.S. money market, long considered the calm anchor of global liquidity, is showing signs of stress. Behind the scenes, a confluence of policy shifts, debt issuance, and liquidity depletion is reshaping the dynamics of how dollars circulate in the system and fuelled the AI bubble.

The First Cracks: Repo Stress and Fed Intervention

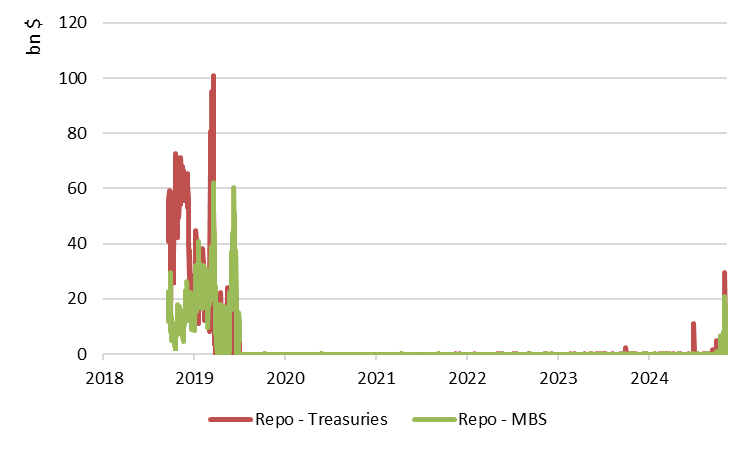

In recent weeks, U.S. banks have started tapping the Federal Reserve's Standing Repo Facility again — a tool designed for emergency funding, as shown in Figure 1. That's not supposed to happen in calm waters. Simultaneously, overnight repo rates — the cost of borrowing cash secured by Treasuries — have jumped, signalling that short-term liquidity is tightening.

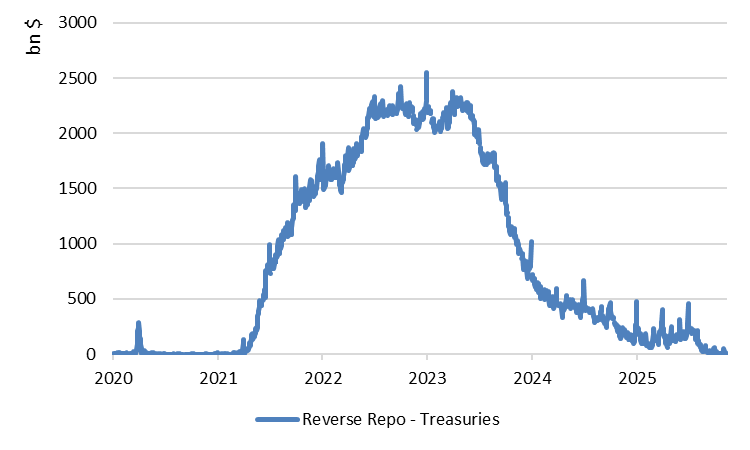

The immediate cause is not mysterious. The once-abundant cash parked in the Fed's Overnight Reverse Repo Facility (RRP) has been draining fast, falling from over $2 trillion in 2023 to nearly negligible levels today. This "cash reservoir" acted as the system's shock absorber. Its depletion means that even small imbalances in supply and demand for funding can now cause noticeable strain.

The Fed's Pivot: From Tightening to Containment

Sensing the risk, the Fed announced at its last FOMC meeting on October 29 that it will end its balance sheet reduction (quantitative tightening) on December 1. Maturing Treasury securities and mortgage-backed securities will now be reinvested into short-term Treasury bills, effectively halting the liquidity drain.

This is not a minor adjustment; it's a tactical pivot. For the first time since the post-pandemic tightening cycle began, the central bank is openly acknowledging that liquidity conditions — not inflation — are now the fragile variable to manage.

The Fed's move is therefore less about boosting the economy and more about stabilising the plumbing — ensuring that the pipes of the system don't freeze just as winter arrives.

Fiscal Pressure: Treasury Floods the Short End

Compounding the problem, the U.S. Treasury has been issuing record volumes of short-term debt. Treasury bills, once a quiet corner of the market, have become a floodgate. This flood has absorbed much of the remaining liquidity from money-market funds, which have been rotating out of the RRP and into these higher-yielding T-bills.

On the surface, that looks harmless — investors are just chasing yield. But structurally, it's draining the last remaining buffer in the system. The Treasury's financing strategy, coupled with the Fed's prior balance sheet runoff, has created a liquidity vacuum that only the Fed can refill.

The Paradox of Safety: Money Market Funds Swell

Meanwhile, investors continue to pile into money-market funds, whose total assets now exceed $7.7 trillion — a record. The irony is sharp: the more investors seek safety, the more they contribute to tightening liquidity, as these funds absorb cash that would otherwise circulate through the banking system.

It's a modern liquidity paradox — the search for safety is making the system less safe.

New Players, New Dynamics

Adding another layer of complexity, stablecoins — such as Tether (USDT) and Circle (USDC) — have emerged as major buyers of U.S. Treasury bills, with a market value in excess of $250 billion. Their presence links the digital-asset ecosystem directly to the core of the global dollar market. It's a new world where crypto demand helps fund U.S. debt, subtly influencing yields at the front end of the curve.

What It Means

The big picture is that the U.S. liquidity cycle has turned fragile.

- The system's cushions — RRP balances, bank reserves, and Fed flexibility — are thinner than at any point since COVID.

- Short-term funding costs are rising.

- The Fed has been forced to quietly shift from tightening to containment.

None of this suggests an imminent crisis. But it does mean the next shock — whether fiscal, geopolitical, or credit-related — will hit a market with far less resilience.

The lesson is familiar but urgent: monetary policy isn't just about rates — it's about liquidity. As liquidity is one of the three elements, with low interest rates and a continuous fiscal stimulus, that have fuelled the current equity bubble (see: How the AI Bubble Was Born from the Ruins of Wall Street), this subtle change in financial conditions matters.

At $46tn, the current bubble is about 6.5 times the size of the dotcom bubble. It is the largest technology bubble on record. It represents 1.5 times the size of the US GDP. The bubble is high and big. What will happen when it bursts?

This article is an extended version of a column originally published in French on Allnews.ch.

← All publications