Europe Is Shifting to a New Fiscal Regime

Defense, energy, industry: Europe is entering an era of structurally higher deficits that will reshape inflation dynamics, interest rates, and asset allocation.

Europe was built on fiscal discipline. Of the five convergence criteria enshrined in the Maastricht Treaty, two are explicitly fiscal. Following the 2010–2012 sovereign debt crisis, fiscal consolidation became the cornerstone of Europe's economic architecture. Reducing deficits was the overriding priority, while monetary policy served as the primary macroeconomic stabilization tool.

That regime now belongs to the past.

Without any explicit institutional rupture, Europe has embarked on a profound transformation of its fiscal framework. Under the pressure of geopolitical, energy, and industrial constraints, public deficits are becoming a structural feature of the European economy. This shift represents a turning point with significant implications for inflation, interest rates, and asset allocation.

The Structural Return of the State and Wider Deficits

The geopolitical shift is the first decisive factor. Russia's invasion of Ukraine in 2022 ended the illusion of a stable security environment. Defence spending has become a strategic imperative. Germany — historically a pillar of European fiscal orthodoxy — has committed to structurally higher military expenditures, with a sustained target above 2% of GDP. This trend extends across the continent and is set to persist.

The energy transition constitutes a second major driver. Reducing dependence on fossil fuels and building resilient infrastructure require massive public investment. These expenditures are inherently structural rather than cyclical.

Finally, the emergence of a European industrial policy through the proposed Industrial Accelerator Act marks a conceptual break. In response to interventionist strategies in the United States and China, Europe is now actively supporting its strategic sectors.

Taken together, these developments signal the durable return of the State as a central actor in economic transformation and structurally higher fiscal deficits as a consequence. Europe's public finance trajectory is likely to converge toward that of the United States.

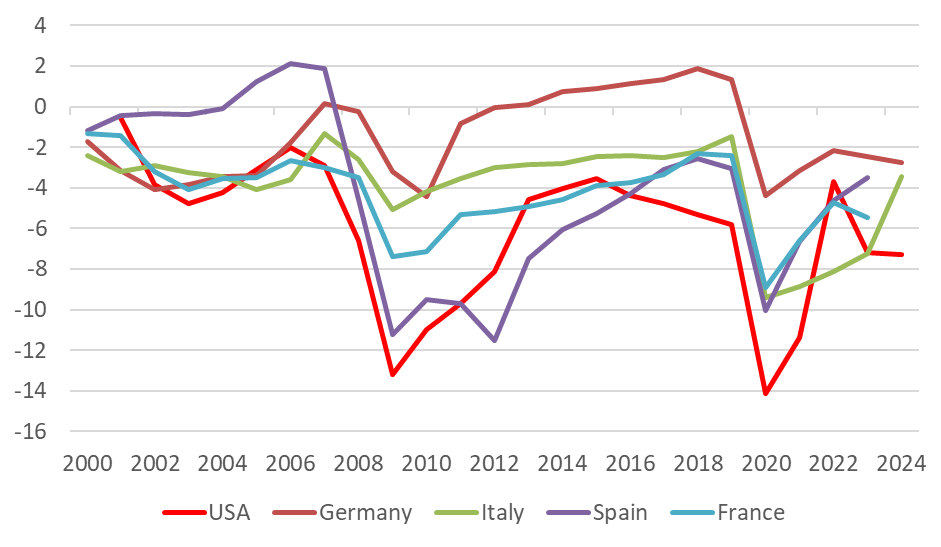

It is worth recalling that the combined debt of Germany, Italy, Spain, and France (see figure 1) accounts for roughly 80% of total euro area public debt. Fiscal policy is thus becoming a core driver of economic dynamics, durably altering the balance between inflation, growth, and interest rates.

Toward Structurally Higher Long-Term Rates

Structural fiscal expansion exerts upward pressure on aggregate demand and inflation. Financing these deficits requires increased sovereign bond issuance, contributing to higher term premia and rising yields.

The post-COVID rate normalization is therefore not merely cyclical adjustment; it represents a shift toward a higher structural floor for long-term rates.

Asset Allocation Implications

In this new environment, sovereign bonds exhibit a different risk–return profile. They revert primarily to being a source of carry rather than a structural engine of capital gains.

Conversely, fiscal expansion supports nominal growth and corporate revenues. Sectors linked to defence, infrastructure, energy, and industrial policy stand to benefit disproportionately from this transformation. Companies exposed to European domestic demand should also be structurally favoured.

This new regime could further enhance Europe's relative attractiveness amid an ongoing rebalancing of global capital flows.

A Historic Turning Point for Investors

The silent fiscal revolution underway marks the end of an era. The regime of fiscal austerity, low inflation, and structurally depressed interest rates is giving way to an environment defined by persistent deficits and higher nominal rates.

For institutional investors, this transformation necessitates a recalibration of strategic asset allocation. Fixed income no longer enjoys the same structural tailwind, while equities may evolve within a more supportive macro backdrop.

As is often the case, regime shifts generate both risks and opportunities. Investors capable of recognizing this structural transition will be best positioned to navigate Europe's new macro-financial environment in the years ahead.

This article is a translation of a column originally published in French on Allnews.ch.

← All publications