Exchange Rate Policy: What About the Euro, the Dollar, and the Renminbi?

In my previous article, "Central Banks' Interest Rate Setting is Dead," I showed that interest rate policy has reached its limits: rates are too low to be cut further to stimulate the business cycle, and too high to sustain public debt. We are on the brink of a shift in monetary and economic policy. Exchange rates are emerging as the new instrument that suits everyone, at the risk of satisfying no one.

Interest Rates and Exchange Rates: Different Levers

The mechanics of exchange rates resemble those of interest rates. An appreciation of the national currency is equivalent to a rate hike. It leads to an economic slowdown and lower inflation. A depreciation of the national currency, like a rate cut, stimulates the economy and inflation.

However, these tools operate through different levers to influence the economy, asset valuation, and inflation.

- Interest rates affect the domestic economy through credit, savings, and investment, while exchange rates influence the external economy through exports and imports.

- Interest rates change the domestic valuation of financial assets, including bonds, equities, and commodities. In contrast, exchange rates affect the valuation of domestic financial assets abroad and foreign financial assets domestically.

- Interest rates influence inflation trends through domestic prices, while exchange rates impact inflation from imported goods.

In summary, interest rates affect the domestic economy, while exchange rates impact the international or non-domestic economy.

What happens at home stays at home — but what happens abroad affects the neighbours! Using exchange rates as a tool of economic and monetary policy causes tensions between economic neighbours. We speak of exchange rate manipulation but not of interest rate manipulation by central banks. This distinction clearly reflects the negative connotation associated with exchange rate policy.

A depreciation of the dollar, for instance, to boost the U.S. economy automatically leads to an appreciation of other currencies and a slowdown in their economies. U.S. international competitiveness thus improves at the expense of the rest of the world, hence the concept of currency wars.

Goals and Constraints

The current world order comprises three major economic blocs, each with its objectives and constraints. The U.S. bloc is the most powerful, as the value of the dollar and U.S. interest rates exert influence on the rest of the world. Its challenges are a high level of public debt and weak international competitiveness, reflected in a chronic trade deficit. A depreciation of the dollar would benefit the U.S.

The Chinese bloc is closely linked to the U.S., as the Chinese government manages the renminbi's exchange rate against the dollar (managed float). One of its main challenges is to boost domestic demand. For comparison, Chinese household consumption accounts for less than 40% of the country's GDP, compared to nearly 69% in the U.S. A gradual appreciation of the renminbi would help China rebalance its economy toward domestic demand.

Finally, the European bloc is caught between the two economic superpowers. Its challenges are primarily political. It must consolidate the Union, i.e., continue economic, political, institutional, regulatory, military, social, and cultural integration to form a strong unified bloc. Faced with Russia, a potentially unifying adversary, it has the opportunity to strengthen around a shared military and budgetary project. The euro plays a minor role in European integration as long as its fluctuations remain orderly.

Louvre, Plaza, Beijing

If the above analysis is correct, a coordinated exchange rate agreement could satisfy all three blocs. Ideally, this would take the form of a formal accord in which the blocs jointly commit to weakening the dollar and strengthening the renminbi to reduce macroeconomic imbalances between the U.S. and China.

This objective has the advantage of being easily observable. First, the dollar-renminbi exchange rate is monitored on a daily basis. Second, central bank statistics (interest rates, foreign exchange reserves) must align with the stated goal. Ultimately, the U.S.-China trade imbalance is expected to start narrowing.

This proposal, more elegant and constructive than the unilateral imposition of tariffs, would also allow the U.S. to "repay" its debt in devalued currency and manage its debt burden, while enabling China to strengthen its domestic sector.

The 1985 Plaza Accord and the 1987 Louvre Accord showed that such arrangements are feasible when parties act in concert. So, when will the Beijing Accord happen?

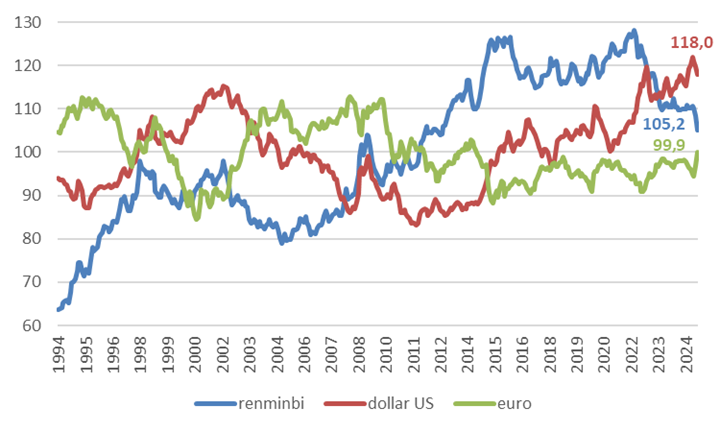

The Euro as Collateral Damage

The real effective exchange rate (REER) measures a country's international competitiveness. A high REER means the currency is strong and the economy is less competitive globally.

According to this metric, the dollar stands at 118, or 18% above its historical average. The renminbi is 5.2% above its long-term average but has depreciated sharply over the past three years (−17.2%), giving China a significant boost in competitiveness. The euro, on the other hand, is close to its long-term average and shows no signs of over- or undervaluation.

Currently, there is no agreement, and to my knowledge, no discussion is underway in that direction. A unilateral dollar depreciation would mechanically lead to a depreciation of the renminbi, due to the strong link between the two currencies. In this scenario, the adjustment is likely to fall on the euro, the collateral victim, which could appreciate and bear the burden of economic rebalancing between China and the U.S.

Conclusion

Exchange rates may well become the monetary policy instrument of the future. But unlike interest rates, their manipulation has immediate international repercussions. In an interdependent world, isolated strategies inevitably lead to economic and political tensions.

The solution may lie in multilateral cooperation: explicit agreements, shared governance, and a common vision. The precedent of the 1980s exists. The question remains whether the political conditions are in place for Washington and Beijing to reach an understanding — and spare Europe from playing the role of bystander and victim in a battle it does not control.

Global monetary and economic rebalancing is inevitable. The euro may well carry a large part of the adjustment.

This article is a translation of a column originally published in French on Allnews.ch.

← All publications