Are Stock Prices Rising or Money Losing Value?

The repo market — or repurchase agreements — lies at the heart of liquidity creation in the United States. According to a recent Federal Reserve study, this market amounts to nearly USD 12 trillion and serves as the intersection where central banks, commercial banks, hedge funds, pension funds, money market funds, investment funds, and corporate treasuries all interact. A central question arises: does this liquidity creation mainly fuel equity market gains, or does it instead erode the value of money?

The Repo Market

The repo market has existed for decades, but it gained systemic importance following the Great Financial Crisis of 2008. Previously, a significant portion of liquidity originated from the interbank market, where institutions lent each other money without collateral, relying on mutual trust. That was the LIBOR era, when trust and liquidity went hand in hand.

The crisis shattered that trust. Basel III regulation replaced confidence in financial institutions with confidence in assets: liquidity now depends on the abundance of high-quality collateral.

The mechanics of repo are simple: an institution holding a safe asset (mainly government or high-rated corporate debt) can temporarily exchange it for cash, committing to repurchase it later at a pre-set date and price. The difference between the initial price and the repurchase price reflects the implicit interest rate — in other words, the cost of short-term liquidity.

Under Basel III, sovereign bonds — especially U.S. Treasuries — are considered the safest assets. Banks hold them in size to strengthen their balance sheets. Other financial players also seek them out, as they provide diversification and immediate liquidity through repo, creating additional leverage in portfolios.

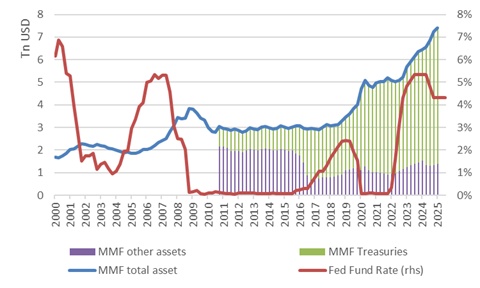

The Role of Money Market Funds

Money market funds play a key role in transforming sovereign bonds into cash equivalents. Under Basel III, these securities share many characteristics with money, while offering yields aligned with the Fed's policy rate.

This combination of attractive returns and abundant Treasuries constantly fuels liquidity creation.

Chronic fiscal deficits ensure a steady stream of new bond issuance in the years ahead. Meanwhile, interest rates are expected to fall with the slowdown in U.S. activity — exacerbated by Donald Trump's unwelcome interference with the Fed. Liquidity creation may decelerate, but it is unlikely to reverse: since 2008, money markets have continued to generate liquidity, even when rates hovered near zero, as the chart below illustrates.

Rising Markets or Falling Money?

According to the Office for Financial Research, a significant portion of this liquidity is utilised by hedge funds to increase their leverage. From late 2022 to today, their use of repo credit has surged from just over USD 1 trillion to USD 2.8 trillion. More than half of these borrowings must be refinanced weekly, and one third daily.

This mechanism partly explains the near-continuous rise in equity markets despite a drumbeat of bad news: wars, trade tariffs, soaring public debt, political uncertainty, and the institutional weakening of the United States. The repo market provides structural support to asset prices.

Paradoxically, the growing valuation of risky assets — such as the Nasdaq, now well above its historical average, or corporate bonds with compressed spreads — has gone hand in hand with rising prices for ultra-defensive assets such as gold and bitcoin.

Gold and bitcoin share a unique characteristic: they are no one's liability and cannot be manipulated. They stand as the antithesis of the financial system's elastic liquidity. Their performance is a reminder that while liquidity props up risky assets, it simultaneously dilutes the value of money. This manifests in the revaluation of "outside" assets and the depreciation of the dollar against other currencies.

Toward a New Strategic Allocation?

These dynamics suggest that a diversified and resilient portfolio may need to move away from traditional equity-bond allocation models. The future could favour a more balanced mix of risky and ultra-defensive assets, better suited to withstand looming economic and monetary challenges. At the centre of this reflection lies the question of the future of the dollar and U.S. debt.

This article is a translation of a column originally published in French on Allnews.ch.

← All publications