Trump's Tariffs risk global dollar shortage

The enormous US trade deficit in 2024 is expected to exceed $1.2 trillion. It is the most significant deficit in the balance of payments in living memory. Against this deficit, the historic surplus of the capital account shows the flip side of international relations: the global financial dependence on the dollar, the United States' number one export commodity. As the two are linked, introducing import tariffs and budget cuts blows global growth and induces a global liquidity shock.

Current account deficit or capital account surplus?

The US trade deficit irritates Donald Trump. In his mercantilist approach, importing more than exporting is a sign of weakness. Reducing economic dependence on foreign countries means re-industrialising the country and restoring America's greatness. Tariffs are unlikely to make it.

The 'problem' is that the United States is the world's leading economic, financial, military and geopolitical power. This exceptionalism is comparable to that of 19th-century England or the Roman Empire, affording the country that holds it an exorbitant privilege: the issuance of the international reserve currency.

To the best of my knowledge, there is no exception to the rule. The country that issues the reserve currency typically incurs a chronic trade deficit, reflecting its dominant position in the world's financial markets.

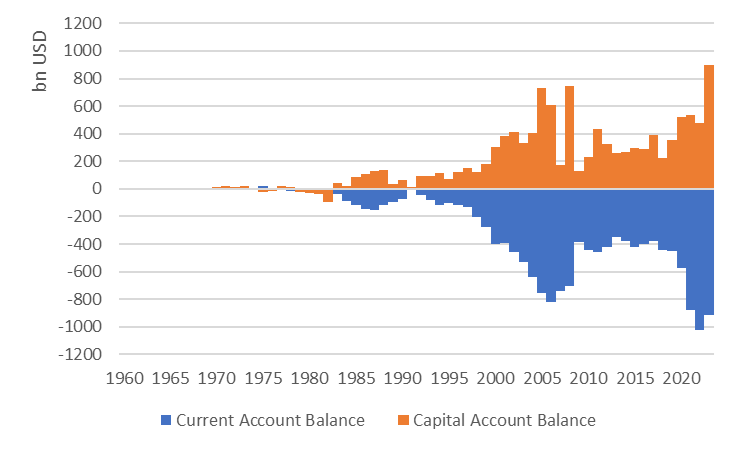

The balance of payments accounts for international trade in goods and services with foreign countries (the current account) and their financing (the capital account). These two balances cancel each other out, as their sum always equals zero. A deficit in the current account is financed by a surplus in the capital account and vice versa.

In the case of the United States, as illustrated in chart 1, the growing current account deficit, reflecting the US trade imbalance, is offset by a chronic capital account surplus.

The question is whether the US is facing a current account deficit, reflecting a problem of economic competitiveness, or a capital account surplus, signalling the supremacy of the dollar in a global financial system that is heavily reliant on it.

The chicken or the egg?

There's obviously no definitive answer to this question, but we do know that one can't go without the other.

The enormous post-war economic boom and the rise of Asia, thanks to outward-looking industrialisation policies supported by institutions promoting globalisation, explain the widening US trade deficit. At the same time, the positioning of the dollar at the centre of the global financial system established in the immediate post-war period through the Bretton Woods agreements made the dollar the international reserve currency. It was in 1971, when President Nixon ended these agreements, that the dollar took off. The end of capital controls and the growing dominance of the United States in the economic, financial, military, ideological and geopolitical spheres did the rest. In all its forms, the dollar was indisputably the international reserve currency and became the most sought-after risk-free financial asset globally. International savings were channelled to the United States, which saw its capital account surplus and prosperity increase. The profits from exporting dollars are far higher than the price at which they are produced and traded on the markets.

No egg, no chicken; no chicken, no egg. As Donald Trump is doing, tackling the trade deficit implies an equally large adjustment to the capital account surplus. Scaling back the US state apparatus and disengaging internationally will improve public debt but reduce US Treasury bond issuance. Yet more than a third of the capital account is financed by government bonds, the risk-free international asset denominated in the reserve currency. These policies are killing the chicken in the egg.

The consequences of a global dollar shortage

Currently, imports from China are taxed at a rate of 20%. On April 2nd, Liberation Day (sic), tariffs of 25% will be imposed on goods and services from Mexico and Canada. These three countries account for 44% of the trade deficit, with imports totalling $1.35 trillion last year.

Next on the list could be the European Union (16.9% of the deficit) with a likely 20% import tariff. Also, Southeast Asian countries are replacing China as a low-cost production hub and flooding the markets with goods. Indonesia and Vietnam have been experiencing double-digit growth in exports for years. Vietnam alone is responsible for more than 10% of the US deficit.

Given the frequent changes of mind of the President of the United States, the conditional remains the order of the day. If such a trade war were launched, the consequences would be far-reaching. Initially, the tariffs are expected to increase US inflation and reduce the nation's purchasing power by approximately $1,200 per household, according to estimates. Soon enough, the reduction in the deficit will lead to a fall in the capital account surplus and a decrease in the number of dollars available internationally, with uncertain effects on exchange rates and interest rates. Only then will the country's reindustrialisation begin, but this will take time because the reallocation of production lines and the construction of new factories, as well as the recruitment of staff (without immigration), will require years. It should also be noted that to re-industrialise, the United States must import raw materials and intermediate goods at a taxed cost. As Musk wrote on X: "The tariff impact on Tesla is still significant".

Regarding the capital account, the dollar-denominated financial commitments of exporting countries typically extend over several years. The fall in their exports and the chronic shortage of dollars will put emerging countries under pressure, and they are likely to be the first victims of the President's mercantilist policies.

However, the dollar will continue to dominate the world's financial markets as long as there is no alternative. However, the end of ideological dominance and the gradual loss of supremacy in other spheres raises the question of the dollar's eventual demise. In this context, it is instructive to note that Chinese dollar-denominated bonds offer a lower yield than US bonds as they are perceived as less risky despite China's significant economic challenges. Things are changing.

This article is a translation of a column originally published in French on Allnews.ch.

← All publications